- YO Edge

- Posts

- Collateral Is the Real Risk

Collateral Is the Real Risk

Why one weak asset can undermine an entire lending market

Exponential.fi

March 10, 2026

Disclosure: This newsletter is for informational purposes only and does not constitute financial advice. Always DYOR before making any investment.

Each week in Edge, we share data-driven insights, highlight risk ratings, and showcase new product updates.

Let’s dive in 👇

What Happens When Collateral Breaks

In lending markets, the yield you see isn’t always where the real risk sits. Many DeFi users evaluate opportunities based on borrow rates, supply APY, or utilization levels. But in most lending protocols, the critical variable is the collateral basket. If the assets backing a market are weak, volatile, or thinly traded, that risk propagates through the entire pool.

Lending markets function by allowing borrowers to deposit collateral and borrow against it. As long as that collateral maintains value, the system remains solvent. But if a collateral asset collapses faster than liquidations can process, lenders ultimately absorb the loss.

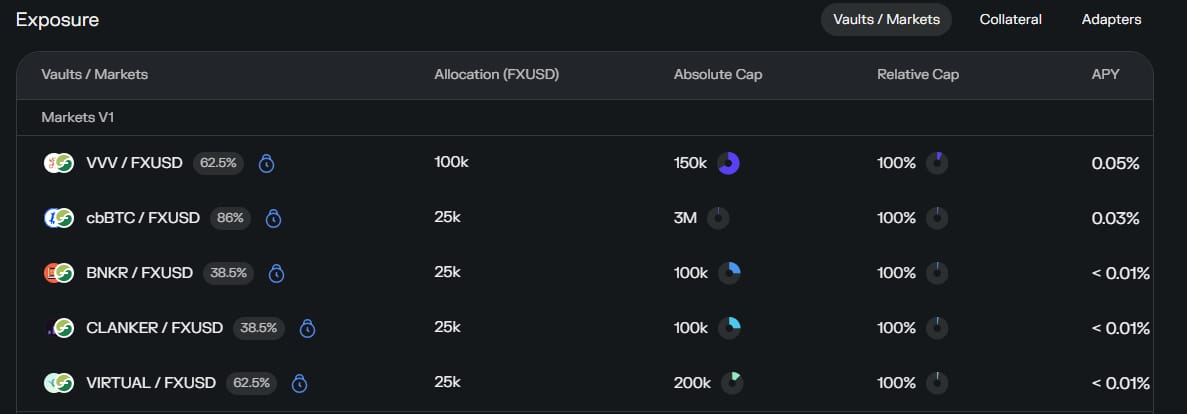

Let’s take this fxUSD market shown above. At first glance, the vault advertises a ~7.7% APY, which is relatively attractive in the current stablecoin environment. But the collateral basket includes in its majority, several niche or low-liquidity assets as shown below.

To understand what this means, let’s imagine CLANKER experiences a sharp price drop. As its value falls, borrowers who used CLANKER as collateral become undercollateralized and are flagged for liquidation. Liquidators then step in to repay the borrower’s debt and seize the CLANKER collateral at a discount but if liquidity is tight, they may struggle to exit positions efficiently. In that scenario, the protocol can end up holding collateral worth significantly less than the borrowed funds and when that happens, the loss is socialized across lenders.

This dynamic is why markets with weaker collateral often display higher yields. The premium exists because lenders are implicitly underwriting the liquidation risk of those assets.

So next time you are looking for DeFi opportunities and you come across lending markets, always make sure you understand what collateral risk you are taking, because you definitely don’t want to lose your money on sketchy collaterals.

yoUSD: Added Aura USDC-GHO on Base and Morpho V2 sky.money USDT on Ethereum. Capital was deployed to new venues chasing the best available risk-adjusted rates. Notably, Aura USDC-GHO on Base marks a new LP strategy type for yoUSD, providing stablecoin liquidity to earn trading fees alongside incentives. Morpho Re Ecosystem USDC was also scaled up as lending demand against reUSD collateral continued to grow. On the exit side, the Morpho PT-sNUSD-4MAR2026/USDC position was largely unwound as it approached its March 4 maturity.

yoETH: Continued scaling into the stETH discount capture strategy. Origin stETH Redemptions more than doubled to 20.13%, making it the vault's largest position as the stETH secondary market discount persists. Capital was freed from Convex ETH+-WETH and Origin superOETHb on Base, both trimmed significantly as yields compressed and allocation was redirected toward the higher-yielding redemption arb.

yoBTC: Added Gearbox Gami WBTC to capture attractive WBTC-denominated incentives on the vault. Capital was rotated out of Morpho Seamless cbBTC on Base and StakeDAO cbBTC-WBTC on Ethereum, with allocation redirected into StakeDAO tBTC-cbBTC and the new Gearbox position for better risk-adjusted returns.

YO Hackathon is live👇

Latest updates in the YOverse 👇

Let us know how we did 👇Provide your feedback on today's issue of the Exponential Edge newsletter. (1 ⭐️ - not useful at all, 5 ⭐️ - extremely useful) |